Analytical Procedures Are Generally Used to Produce Evidence From

In forensic auditing specific procedures are carried out in order to produce evidence. Evidence may also.

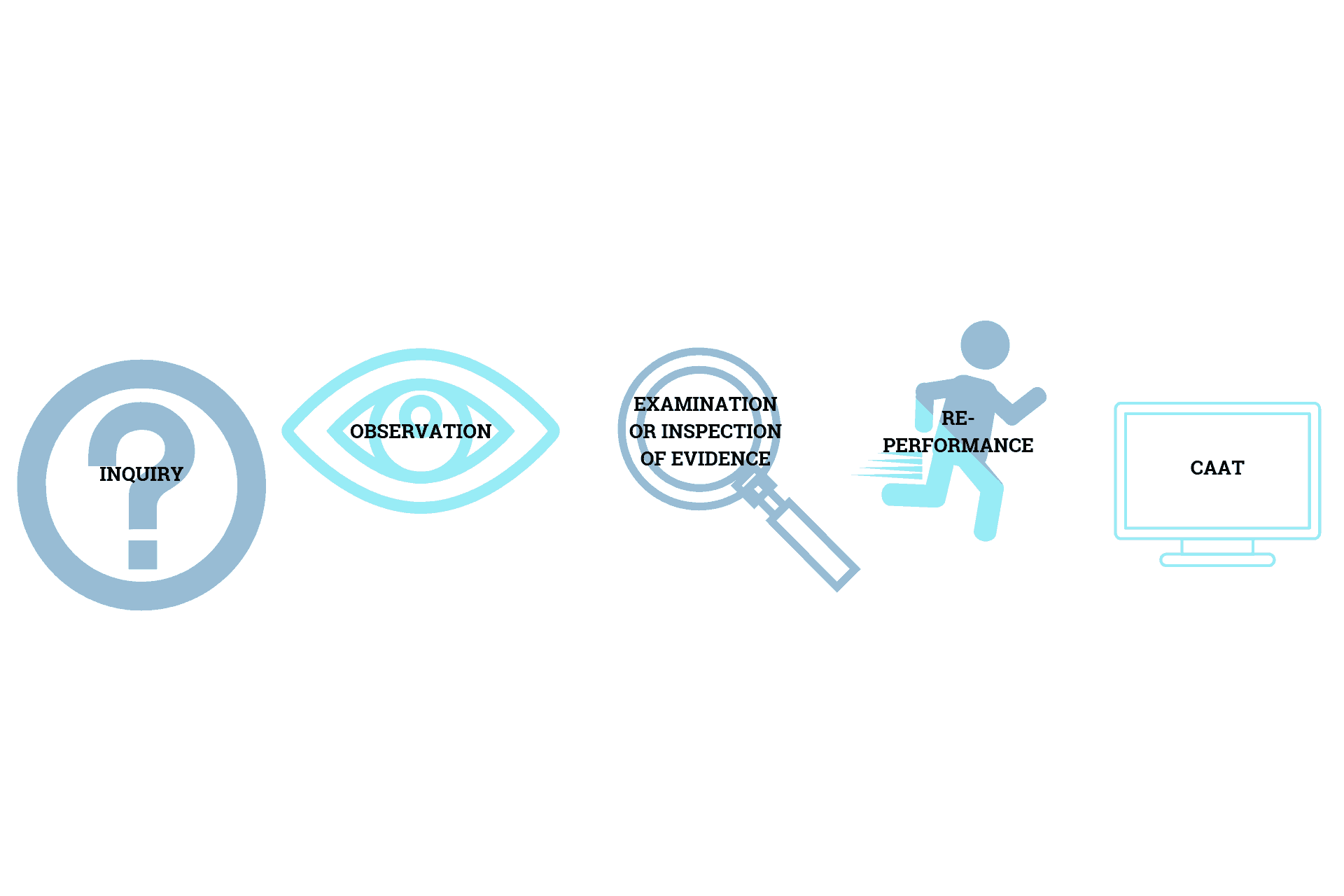

5 Types Of Testing Methods Used During Audit Procedures I S Partners

Form an independent expectation about an account balance or financial relationship.

. Gather evidence from tests of details to corroborate financial statement assertions. These tools generally include analysis of trends ratios or relationships between the information in the financial statements. Detailed examination of external external-internal and internal documents.

Identify differences between expected and reported amounts. C Relationships among current financial balances and prior balances forecasts and nonfinancial data. Analytical procedures are generally used to produce evidence from.

Relationships among current financial balances and prior. Here the auditor develops an expectation of an account balance or financial relationship. Audit techniques and procedures are used to identify and to gather evidence to prove for example how long have fraudulent activities existed and carried out in the organization and how it was conducted and concealed by the perpetrators.

Analytical procedures are generally used to produce evidence from. B Detailed examination of external externalinternal and internal documents. Analytical procedures are generally used to produce evidence from a.

Physical observation of inventories. Analytical procedures are the procedures that use by auditors to obtain the audit evidence so that they could assess and evaluate the financial information that presents in the financial statements based on the concept that the financial information has plausible relationships with the others financial and non-financial information or data. Accounting questions and answers.

1 to corroborate substantive tests of details for the same assertion thereby enabling a reduction in the scope of the tests of details for example by lowering. Analytical procedures are generally used to produce evidence from a. During fieldwork auditors can use analytical procedures to obtain evidence sometimes in combination with other substantive testing procedures to identify misstatements in account balances.

Expectations are formed by identifying. Final analytical review required by ISA 520. Relationships among current financial balances and prior balances forecasts and nonfinancial data.

Confirmations mailed directly to the auditors by client customers. Analytical procedures are generally used to produce evidence from a. A Confirmations mailed directly to the auditors by client customers bPhysical observation cRelationships amont current financial balances and prior balances forecasts and nonfinancial data d Detailed examination of external external-internal and internal documents.

Detailed examination of external external-internal and internal documents b. Performing analytical procedures generally follows this four-step process. Analytical procedures are used as substantive procedures when the auditor considers that the use of analytical procedures can be more effective or efficient than tests of details in reducing the risk of material misstatements at the assertion level to an acceptably low level.

Confirmations mailed directly to the auditors by client customers. Physical observation of inventories. Confirmations mailed directly to the auditors by client customers.

Analytical procedures are generally used to produce evidence from. Analytical procedures are generally used to produce evidence from a. Analytical procedures are a type of evidence used during an audit.

Relationships among current financial balances and prior. Relationships among current financial balances and prior balances forecasts and non-financial data c. Relationships among current financial balances and prior.

A primary objective of analytical procedures used in the final review stage of an audit is to a. As a substantive test to obtain audit evidence about particular assertions related to account balances or classes of transactions. Analytical procedures generally follow these five steps.

Physical observation of inventories. Confirmations mailed directly to the auditors by client customers. Detect fraud that may cause the financial statements to be misstated.

Relationships amount current financial balances and prior balances forecasts and nonfinancial data d. Forecasts and nonfinancial data. These procedures can indicate possible problems with the financial records of a client which can then be investigated more thoroughly.

In this case auditors perform data analysis to examine whether it is consistent with other relevant information and whether the fluctuation is within their expectation. Confirmations mailed directly to the auditors by client customers. Physical observation of inventories c.

Confirmations mailed directly to the auditors by client customers. Investigate the most probable cause s of any discrepancies. Physical observation of inventories.

Identify account balances that represent specific risks relevant to the audit. The current standards permit but still do not require the use of analytical procedures as substantive tests but auditors commonly use them to achieve audit efficiency in two ways. Confirmations mailed directly to the auditors by client customers b.

Analytical procedures are generally used to produce evidence from Confirmations mailed directly to the auditors by client customers. Physical observations of inventories. And As an overall review of the financial information in the final review stage of the audit.

A Confirmations mailed directly to the auditors by client customers. 0 out of 000 points Analytical procedures are generally used to produce evidence from O ³ O O O O Relationships among current financial balances and prior balances forecasts and nonfinancial data. In other words analytical procedures are used throughout the audit engagement in audit planning execution and review.

Relationships among current financial balances and prior balances forecasts and nonfinancial data. Developing an independent expectation helps the auditor apply professional skepticism when evaluating reported amounts. Evaluate the likelihood of material misstatement.

Analytical procedures are generally used to produce evidence from. Analytical procedures are generally used to produce evidence from. It can also include determining the relationship between financial and non-financial data.

Confirmations mailed directly to the auditors by client customers. Analytical procedures are the processes of evaluating financial information through trend ratio or reasonableness of data in relation to other financial and non-financial data. A b Detailed examination of external externalinternal and internal c Relationships among current financial balances and prior.

Analytical procedures include different processes through which auditors can analyze the financial statements of a company. This can help reduce the risk that misstatements will remain undetected.

Chapter 7 Audit Evidence

Chapter 7 Audit Evidence

Audit Procedures Types Assertions Accountinguide

Comments

Post a Comment